eFX Apex

The Institutional-Grade Data Hub

- Plus: Discretionary Trades

- Edge: Sentiment Trades

- Alpha: Systematic Trades

- Apex: Full Big Data Stream

SEB Research previews the July ECB policy meeting on Thursday.

"Unchanged policy rates...ECB will reiterate its data-dependent approach, not precommitting to a particular rate path, but signaling readiness to act if needed (implying further possible rate hikes)," SEB notes.

"The energy price development since the latest monetary policy meeting has been favorable and most members have recognized the possibility of not stressing the next move. However, many members see a rate hike as highly likely, but improvements of the energy shock may call this off," SEB adds.

The dollar was mixed on Wednesday, as higher Treasury yields and oil prices amid renewed verbal threats between the U.S. and Iran weighed on haven currencies, while DAX gains and cross-related flows underpinned the euro. A dearth of U.S. data kept the focus on geopolitics, with equity markets mixed as investors prepared for second-quarter results from Alphabet GOOGL.O and Tesla TSLA.O, the first "Magnificent Seven" megacap companies to report after the bell for fresh evidence that these companies' multibillion-dollar investments in AI are paying off. President Donald Trump warned the U.S. would strike Iranian infrastructure if Iran attacked shipping in the Strait of Hormuz, while Tehran vowed to target U.S.-linked regional infrastructure in response. Trump envoys Steve Witkoff and Jared Kushner discussed diplomacy with Ukraine President Volodymyr Zelenskiy, who described the talks as constructive. Germany will launch a state-backed fund to invest directly in defense startups. U.S. Trade Representative Jamieson Greer hopes to reach interim trade deals with Mexico and Canada this year ahead of broader USMCA changes in 2027.

The Norwegian krone topped G10 gains, while the Swiss franc lagged. DXY vols stayed near YTD lows amid subdued turnover, though yen vols firmed on intervention fears and Bank of Japan policy uncertainty. EUR/USD edged higher on risk-friendly flows and EUR/JPY strength, but the broader technical outlook remains bearish while below its 10- and 21-DMAs near 1.1412-20.

EUR/CHF notched a third consecutive gain to its highest since late January, with the move supported by bullish momentum above its upper Bollinger. GBP/USD was under pressure after a fifth straight session of lower highs and lows, with rising oil prices, U.K. fiscal concerns and elevated gilt yields keeping the bias bearish below 1.34. AUD/USD remained constructive above key moving averages despite USD strength, with dip-buying and rising risk assets helping preserve the broader bullish bias. USD/JPY remained bullish above 163, supported by higher yields and improving momentum, though intervention risks were increasing as a BOJ meeting approaches.

Treasury yields were up 1 to 4 basis points as the curve flattened. The 2s-10s curve was down about 1 basis point to +35.0bp.

The S&P 500 was flat in mixed market.

WTI oil rose over 3% to a six-week high.

Gold rose 1.5% while copper fell 0.9% as the CNH weakened.

Heading toward the close: EUR/USD +0.11%, USD/JPY -0.04%, GBP/USD -0.01%, AUD/USD -0.05%, DXY -0.05%, EUR/JPY +0.10%, GBP/JPY -0.01%, AUD/JPY -0.07%.(Editing by Burton Frierson Robert Fullem is a Reuters market analyst. The views expressed are his own)

• NY opened near 0.6995 after 0.7013 traded overnight, the pair initially extended its drop

• Broad-based USD buying, US yield gains & USD/CNH rally sank AUD/USD

• The pair neared the rising 10-DMA, traded 0.6980, buyers then emerged

• Rallies in gold, silver and equities helped lift AUD/USD briefly above 0.7000

• The pair neared 0.6995 late in the session, it traded down -0.07% in NY's afternoon

• A daily doji formed which suggest there is indecision by investors

• AUD/USD's hold above the 10-, 21- & 200-DMAs and rising

monthly RSI are bull signs

audusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

Deutsche Bank previews the July ECB policy meeting on Thursday

"A pause in July is expected. Current oil prices remain below 11 June levels, and the June HICP inflation data, which came in softer than expected, cast some doubt on the rapid emergence of indirect inflation. Furthermore, our June dbDIG survey indicated a complete unwinding of the initial energy shock's impact on household inflation expectations. Waiting until September will provide the ECB with two additional HICP prints and updated staff forecasts, enabling a more informed decision," DB notes.

"We continue to anticipate a second and final hike to 2.50% in September. In the July press conference, we expect the ECB to maintain neutral communications. This implies no explicit forward guidance, emphasizing a data- dependent, meeting-by-meeting approach without pre-committing to a specific policy path. While the communication will be neutral, we believe the ECB's tone on inflation will still convey a hawkish stance, consistent with a further 25bp hike in September being highly probable," DB adds.

• EUR/GBP bid tone builds, reclaiming 200-hour MAs and shifting near-term momentum higher

• Initial topside capped at 0.8540, clean break needed to re-open 0.8600 handle

• UK CPI miss reinforces BoE “on hold” narrative, weighing on GBP near-term

• ECB seen on hold in July but retaining hawkish bias, offering relative EUR support

• Dips well supported into 0.8480–0.8500 zone, stronger base

at 0.8455 (15 July low)

EURGBP hourly chart

Justin McQueen is a Reuters market analyst. (The views expressed

are his own).

((Email: ))

MUFG Research on the scope for another wave intervention by Japan's MoF.

"The USD/JPY rate has hit the highest level since December 1986 and what is noticeable about that is the lack of attention this is now getting. With the move a slow grind and with broader G10 and USD/JPY volatility levels so low the MoF’s justification for intervention is simply not there. The 1-month implied volatility in USD/JPY fell below 6% last week for the first time since February 2022," MUFG notes.

"We did get a comment from Finance Minister Katayama who laid the blame for yen weakness solely on the worsening situation in the Middle East but added that “we will take appropriate and bold action at any time, should the need rise”. That’s an interesting caveat – “should the need arise” which clearly suggests a lower sense of urgency than at previous times when intervention took place. There is certainly a shift in urgency in Tokyo which may point to resignation and reluctant acceptance of allowing the yen to weaken as long as the pace of the move is gradual," MUFG adds.

EUR/USD ticked up on Wednesday but stayed locked in its downtrend from the May 11 high, trading below both the 10- and 21-day moving averages—technical signals that are bearish in their own right. More troubling for investors, though, is that the pair isn't capitalizing on a notable rise in euro zone interest rates, suggesting underlying weakness.

The catalyst for those higher euro zone rates has been the sharp rally in oil prices following the escalation of the U.S.-Iran conflict, which raises the risk of hotter euro zone inflation. This has pushed euro zone rates markets to price in a more hawkish ECB stance: the German 2-year government yield

broke above a bull pennant pattern that had been forming since March, while June 2027 Euribor futures dropped below the base of a bear pennant. Both developments point to markets anticipating the ECB may need to raise rates.

Yet despite these upward moves in euro zone rates, EUR/USD hasn't been able to rally—it's actually trading slightly lower than when the U.S. resumed bombing Iran on July 8. This suggests investors are focused more on the U.S. side of the equation, with rising U.S. rates reflecting growing bets that the Fed could hike rates later this year.

Given this dynamic, EUR/USD is likely to struggle to sustain

any meaningful rally. A genuine turnaround would probably

require a downward shift in U.S. inflation expectations, which

could prompt markets to price in a less-hawkish Fed.

june2027euribor

de2yt

eurusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

Bank of America Global Research sees NZD upside vs GBP and EUR over the coming weeks.

"A more hawkish RBNZ stands in contrast to our expectations for the rest of the G10 commonwealth countries makes it an attractive G10 long. This is compounded by significantly short speculative market positioning in NZD," BofA notes.

"We would generally prefer NZD shorts funded in GBP or EUR. This week also saw the official transition to the Burnham government in the UK, which has already brough on some financial market noise, injecting more 2-way risk into gilts and the pound. As it relates to the EUR, the NZD is attractive on a vol-adjusted carry basis, is bi-laterally insulated from potential energy terms-of-trade deterioration, and stands to benefit from higher agricultural and metals outlook," BofA adds.

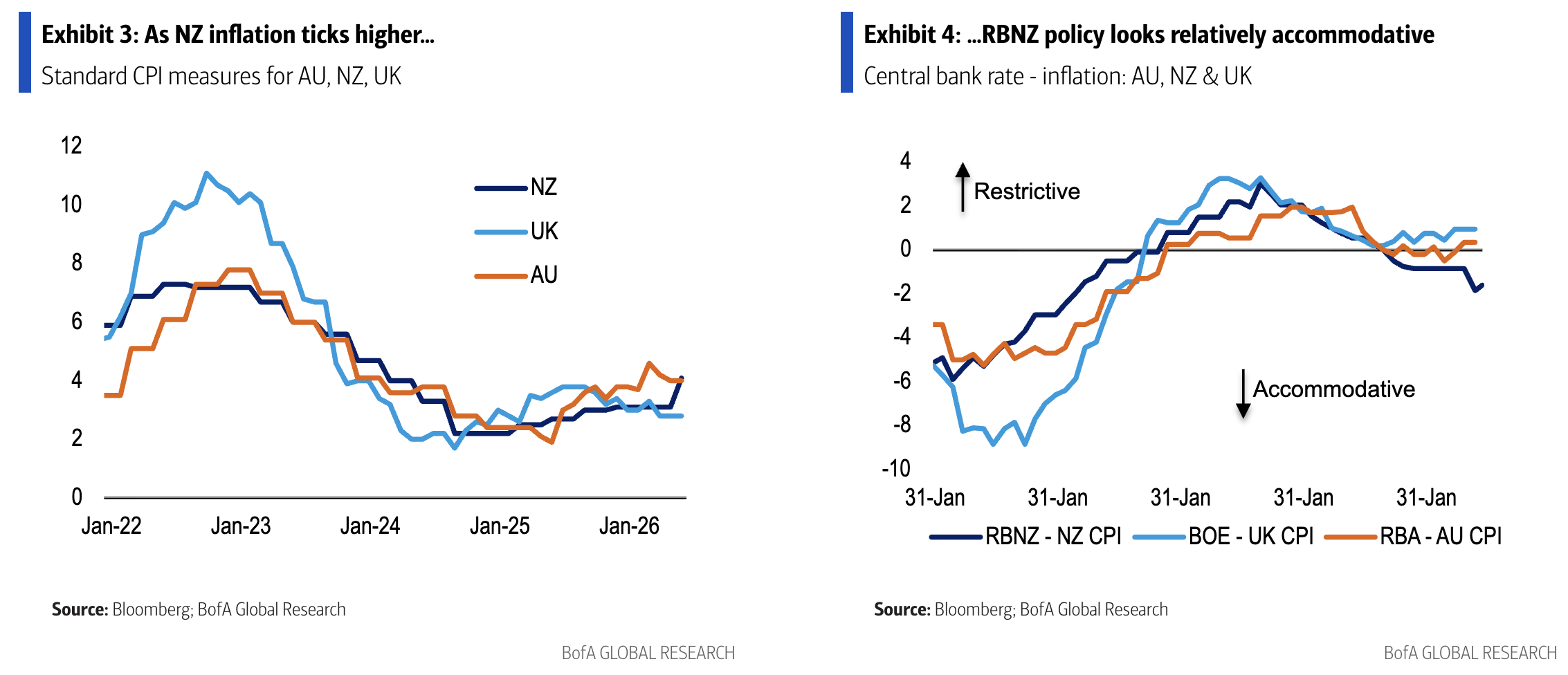

Goldman Sachs Research reviews New Zealand's 2Q CPI and adds a December hike to its RBNZ rate call.

"New Zealand's headline CPI increased 1.5% qoq in 2Q2026, with the year-over-year rate accelerating 100bp to 4.1%yoy. The outcome was above both our expectations and the RBNZ's updated July forecast (GSe/RBNZ: +3.9%yoy; BBG: +4.0%yoy)," GS notes.

"Against the backdrop of renewed upward pressure on oil prices, we expect today's CPI data will reinforce the RBNZ's recent hawkish reaction function reset. We continue to expect the RBNZ to hike the policy rate in September (+25bp to 2.75%) but now expect a final 25bp hike at December's meeting to 3.00% - following a period of assessment, the 7 November election, and with updated forecasts on hand," GS adds.

USD/JPY is pushing 40-year highs, trading above 163.00, even as sources suggest the BOJ could be open to raising rates faster than its usual six-month cadence. That hawkish signal has barely dented price action, with the pair holding higher levels regardless. Options markets are flagging the intervention risk even if spot isn't. Sub-1-month 25 delta risk reversals are holding a strong premium for JPY calls over puts — the right to buy JPY versus sell JPY. That skew is the options market's way of pricing a higher probability of a sharp downside (JPY-positive) shock than the calm spot chart and low implied volatility suggest.

Separately, realised volatility remains very low — and that's a double-edged sword for option buyers. Cheap realised vol means a straightforward option can quickly become an expensive way to protect against intervention: if spot keeps drifting quietly and realised stays subdued, the holder ends up bleeding premium for a scenario that never materialises.

A cheaper alternative is to buy out-of-the-money JPY calls — i.e., the right to sell USD/JPY (buy JPY) at a strike well below current spot. The further the strike sits from spot, the lower the upfront premium, since there's less intrinsic value and a lower probability of finishing in-the-money under normal drift. But should Japanese authorities step in to intervene, USD/JPY has historically been capable of dropping five big figures or more within minutes — more than enough to bring even a deep OTM strike into play.

Example: With USD/JPY spot at 163.00 and 1-month implied volatility at 6.2, a 1-month 163.00 JPY call — allowing the holder to sell USD/JPY at 163.00 at expiry — costs around 137 pips. That's the maximum loss if nothing happens and the option expires worthless.

Compare that with a 1-month 160.00 JPY call, which costs just 49 pips. The lower premium means less capital at risk if spot simply grinds higher and intervention never comes, yet the structure still leaves the holder positioned to profit from a sharp intervention-driven drop, since a move of that magnitude should easily push spot through 160.00.

In a market where realised volatility is low but the intervention tail-risk is real, sizing the hedge via strike selection — trading a bit of protection for a much smaller premium outlay — looks the more efficient way to stay covered without paying for volatility that isn't showing up.

Related — FX options wrap — How low can vol premiums go?

USD/JPY implied vs realised vol

USD/JPY 25 delta option risk reversals

(Richard Pace is a Reuters market analyst. The views expressed

are his own)

Gold, considered both a safe haven and an inflation hedge, should thrive under current conditions. Because rallies in the precious metal tend to precede dollar declines, the prospect of a significant increase in gold prices is reason to anticipate larger moves in currencies. The escalation of conflict in the Middle East, which has lifted oil and gas prices, along with the enduring war in Ukraine and a global trade war that looks set to intensify with new U.S. tariffs, should support safer assets.

This backdrop seems ideally suited for gold, following a correction from near $5,600 to just below $4,000/oz, which has alleviated overbought conditions and reduced the number of wagers that had been restraining gold's rise. Gold is freer to rise amid an uncertain environment that has inflation worries at its heart.

The precious metal, which rose almost $3,000/oz between January 2025 and January 2026, has great potential to rise again, weighing on the dollar index, which plunged by around 15% over the same period. With speculators sitting on one of the largest-ever bets on a rising dollar, a slide led by gold now could be far more damaging for the U.S. currency.

Gold and betting

(Jeremy Boulton is a Reuters market analyst. The views expressed

are his own)

• Shares of Hochschild Mining up about 2.5% at 456.8p

• Co posts Q2 attributable production of 76,231 gold equivalent ounces, up 0.8% from last quarter; remains on track to meet its 2026 production guidance of 300,000–328,000 gold equivalent ounces

• Inmaculada and San Jose generated robust cash flow in Q2, while Mara Rosa improved production due to better plant stability and progress in its operational turnaround

• Gold prices at 2-week highs on Wednesday, supported by technical buying as investors monitor escalating Middle East conflict and ahead of next week's U.S. Fed meeting

• Including session gains, shares are down about 10.69% YTD

(Reporting by Jahanvi Kothari in Bengaluru)

• Shorter dated expiry GBP related FX option implied volatility is under the cosh early Wednesday

• Sales of 1-week vol from the mid 5s and 1-month at 5.9 and 5.85, plus various sub 1-month strikes

• Implied vol sales that cheapen option premiums typically indicate expectations of low realised volatility

• That fits as GBP eases now Andy Burnham is UK PM and cabinet picks remove FX surprise risk

• GBP/USD has dropped back from July 15 high since May at 1.3556 to the middle of long term ranges in the mid 1.33's

• For benchmark 1-month vol, 5.5 marks the recent and 2026 low — a likely support level

• Related comment - FX option pricing nears its limits

GBP/USD FXO implied volatility

(Richard Pace is a Reuters market analyst. The views expressed

are his own)

• USD/JPY extended 40-year highs above 163.00 on Tuesday, pushing deeper into intervention risk territory

• Options have seen downside strike premiums increasing in value compared to upside strikes - reflects intervention risk

• Sub 1-month 25 delta risk reversals marginally firmer for JPY calls over puts - the right to buy JPY vs sell JPY

• Option implied volatility increased with spot - benchmark 1-month rising from 4-year lows near 5.95 to 6.5 (now 6.3)

• A lack of follow through and continued low realised

volatility continues to weigh on implied vol across all currency

pairs

USD/JPY 25 delta option risk reversals

(Richard Pace is a Reuters market analyst. The views expressed

are his own)

• FX option strikes expire at 10am New York/14:00 GMT on Wednesday July 22

• EUR/USD: 1.1350-60 (802M), 1.1375-85 (1BLN), 1.1395 (450M), 1.1400 (3.6BLN), 1.1430 (430M), 1.1455-65 (583M)

• USD/CHF: 0.8065-75 (1BLN), 0.8100 (292M), 0.8200 (267M)

• EUR/GBP: 0.8500 (247M), 0.8550-60 (290M). GBP/USD: 1.3500-05 (364M)

• AUD/USD: 0.6900 (1.8BLN), 0.6975-80 (448M), 0.7040-45 (610M)

• NZD/USD: 0.5825 (352M), 0.5840 (380M). AUD/NZD: 1.2000 (300M)

• USD/CAD: 1.4075 (666M), 1.4100 (210M), 1.4115-25 (502M)

• USD/JPY: 162.50 (1BLN), 163.00 (2BLN), 163.50 (895M), 163.75 (400M)

• AUD/JPY: 113.50 , 114.00 (546M)

• Tuesday's FX options wrap - How low can vol premiums go? (Richard Pace is a Reuters market analyst. The views expressed are his own)

• Shares of Australia's Westgold Resources rise as much as 6.4% to A$4.86

• Stock on track for its strongest intraday trading session since July 3, if moves hold

• Gold producer posts FY26 gold production of 387,354oz, above FY26 forecast range of 345,000 to 385,000oz

• Company says it has not experienced any diesel supply disruptions, retains contingency plans to manage potential supply disruptions due to Middle East geopolitical developments

• Nearly 5.0 million shares trade hands, about 1.5x the 30-day average volume

• Stock down 25.2% YTD, including current session's moves

(Reporting by Subhalakshmi Dey in Bengaluru)

• USD/JPY 163.03-22 EBS in Asia, consolidating gains to 163.24 yesterday

• High yesterday best in 40 years, specs eyeing 164.00, 165.00 tests now?

• Japan FinMin Katayama jaw-boning, threat of intervention helped cap for now

• That said, some feel MOF reluctant to act with USD broadly bid

• Factors include Middle East war and crude price re-rise, higher US yields

• Support on dips from $2 bln option expiries today at 163.00

• Upside spot action likely contained for now by 163.07-80 $1.6 bln expiries

• Support on dips from 163.00 then hourly Ichi kijun at 162.85, 100-HMA 162.50

• Support too from foreign ccy hedging of fresh Nikkei buys, importer buys

• AUD/JPY and NZD/JPY shine some more on suspected additional carry trades

• AUD/JPY 114.05-39 and best since 114.91 June 2, 115.00 test seen possible

• Up with hourly Ichi kijun at 114.06, cloud 113.50-71 below, 100-HMA 113.67

• A$546 mln in option expiries today at 114.00 strike likely supportive

• NZD/JPY 94.94-95.22, below 95.42 yesterday, best since 95.41/42 May 29/Jun 1

• Clean break above 95.50 projects test of 96.00, 94.40 July 17, 2024 June

• EUR/JPY buoyant with JPY under the gun again, Asia 186.00-04 EBS

• Above 185.92 hourly Ichi tenkan, cloud 185.68-73 below, 100-HMA 185.66

• CHF/JPY on hold, 200.57-89, below 201.28-95 daily Ichi cloud, 201.44 100-HMA

• In 200.63-84 hourly Ichimoku cloud, 100-HMA 200.80 in cloud, 200-HMA 200.52

• GBP/JPY 218.05-39 and tad heavy, down from 219.60 high July 15

• Into thinning 218.30-38 hourly cloud, between 217.89/218.48 200/100-HMAs

• Related comment , also , on Japan trade

USD/JPY hourly:

AUD/JPY daily:

NZD/JPY daily:

(Haruya Ida is a Reuters market analyst. The views expressed are his own)

• Australian gold stocks rise as much as 3% in early trade, while the broader benchmark trades up 0.4%

• Sub-index logs the largest intraday pct jump since July 16

• Gold prices rose overnight on hopes of a diplomatic breakthrough between the U.S. and Iran, which could ease energy prices and temper expectations of a hawkish Federal Reserve [GOL/]

• Index leaders Northern Star Resources and Evolution Mining rise 3% and 4.5%, respectively

• YTD, AXGD down 18.7%, including the day's moves, lagging

behind a 1.3% gain on the AXJO

(Reporting by Nikita Maria Jino in Bengaluru)

July 22 (Reuters) - Japan's Ministry of Finance has been conspicuously absent regarding the ordering of Bank of Japan FX intervention despite USD/JPY rallying to as high as the 163 handle Tuesday. Barring action Wednesday, a new equilibrium is likely on 163, following those at lower handles beginning from 157 after interventions in late April and early May . Although there has been recent news of Finance Minister Satsuki Katayama and MOF taking a new tack on FX policy and towards the BOJ, there is little evidence this is actually the case. Tokyo pundits suggest the Takaichi administration's policies remain tied to 'Abenomics', which had as its two pillars a weak yen and loose monetary policy. Despite the new Takaichi economic blueprint giving assurances of BOJ independence , it appears that pressure on the central bank to hold off more rate hikes as long as possible hasn't changed. Barring actual FX action to take USD/JPY lower and/or BOJ action on rates, the USD/JPY uptrend in place from the April 22, 2025 low of 139.89 will likely continue, albeit with intermittent retracements. Tokyo players and especially Japanese importers fret USD/JPY will soon test 165, where massive importer option barriers have been placed. Taking out of these barriers will knock out lower level buy-side contracts, forcing this bloc to buy even more U.S. dollars at spot prices .

Related comments , , , , , , also ..

USD/JPY:

(Haruya Ida is a Reuters market analyst. The views expressed are his own. Editing by Ewen Chew)

• Lack of Japan FX intervention allowed USD/JPY to pop higher to 163 handle

• Yesterday saw 162.44 to 163.24 rise, Asia so far today 163.18-22 EBS so far

• Renewed US-Iran hostilities, closing of Red Sea too, higher US rates factors

• Wall St rally, expectations of Nikkei rally, foreign currency hedges too

• USD/JPY highest in 40 years, next resistance 164.00, then 164.74 in Nov '86

• Market moving ever closer to especially massive 165.00 option barriers

• In expiries today, $2 bln at 163.00, supportive, also 163.07-80 $1.6 bln

• Tech support on dips from 163.10 hourly Ichimoku tenkan

• Option-related bids pre-163.00, hourly kijun 162.84, cloud 162.37-46

• Barring MOF-ordered FX intervention, USD/JPY to see new equilibrium on 163

• Related comments , , ,

• Also , on Middle East ,

• US markets , , ,

• On "new" Trump tariffs , for more click on [FXBUZ]

USD/JPY:

Nikkei 225:

NYMEX crude oil futures:

(Haruya Ida is a Reuters market analyst. The views expressed are his own)

• AUD/USD opens unchanged after failing to sustain a rise to a 1-month high

• Rally thwarted by USD strength; DXY at 1-week high as Treasury yields climb

• Iran war escalation and elevated oil prices boost Fed rate hike bets

• U.S.-10 year yield rises to 2-mth high on inflation concerns, capping AUD

• AUD outperforms as stocks, metals rally; AUD/JPY +0.45%, hits 7-week high

• But failure to sustain break of 0.7023, 38.2% Fibo of May-June drop bearish

• More resistance at 0.7050, 0.7070-75; support 0.6985-90, 0.6960-65

• Tuesday range 0.6993-0.7027

AUD:

(Krishna Kumar is a Reuters market analyst. The views expressed are his own.)

Danske Research maintains a bearish bias on EUR/CHF over the medium-term.

"Over the past month, EUR/CHF has edged higher to above the 0.92 mark, with the ECB delivering hikes and the Swiss National Bank (SNB) pushing back on hike expectations. We remain bearish on EUR/CHF and think the environment continues to favour a stronger CHF. We target the cross at 0.90 in 6-12 months," Danske notes.

"The SNB remains firmly on hold with its policy rate at 0% and we expect this to remain the case. At its most recent meeting, the SNB highlighted that underlying inflationary pressures remained broadly unchanged, despite headline inflation edging slightly higher. This is only further underpinned by the strong CHF and Switzerland’s favourable energy mix. We think this will keep the SNB from hiking rates. Combined with strong fundamentals, we think persistently diverging price levels favour a stronger CHF via the PPP. Additionally, a global investment environment characterised by weak global growth and elevated uncertainty benefits CHF. " Danske adds.

(Corrects typo in bullet #2)

• GBP$ soft in NorAm afternoon trade, -0.34% at 1.3385; NY range 1.3420-1.3360

• UK employment data marginally lower, unemployment a touch higher holds no sway on rates

• Wednesday's UK CPI moves into focus, headline and core both seen a touch lower

• UK data aside, lingering Mideast tensions rising oil hints at steady UK inflation

• UK politics also in mix; post regime change UK fiscal angst higher; UK 10-yr gilt abv 5%

• GBP$ supt 1.3374 falling 55-DMA, 1.3360 Tuesday low,

1.3348 50% Fib of 1.3140-1.3556

GBP Chart:

(Paul.Spirgel is a Reuters market analyst. The views expressed

are his own)

ANZ Research likes buying the dips in EUR/GBP.

"EUR/GBP fell below 0.85 last week, breaking below key longterm support. However, momentum indicators are becoming stretched, with the 14-day RSI near 20, in oversold territory. Also, one-month risk reversals have fallen but remain above zero, suggesting options markets are not yet signalling a structurally GBP-bullish outlook," ANZ notes.

"We see an opportunity to buy on dips. Initial support lies at 0.842, with stronger resistance near the 50-dma at 0.862," ANZ adds.