eFX Apex

The Institutional-Grade Data Hub

- Plus: Discretionary Trades

- Edge: Sentiment Trades

- Alpha: Systematic Trades

- Apex: Full Big Data Stream

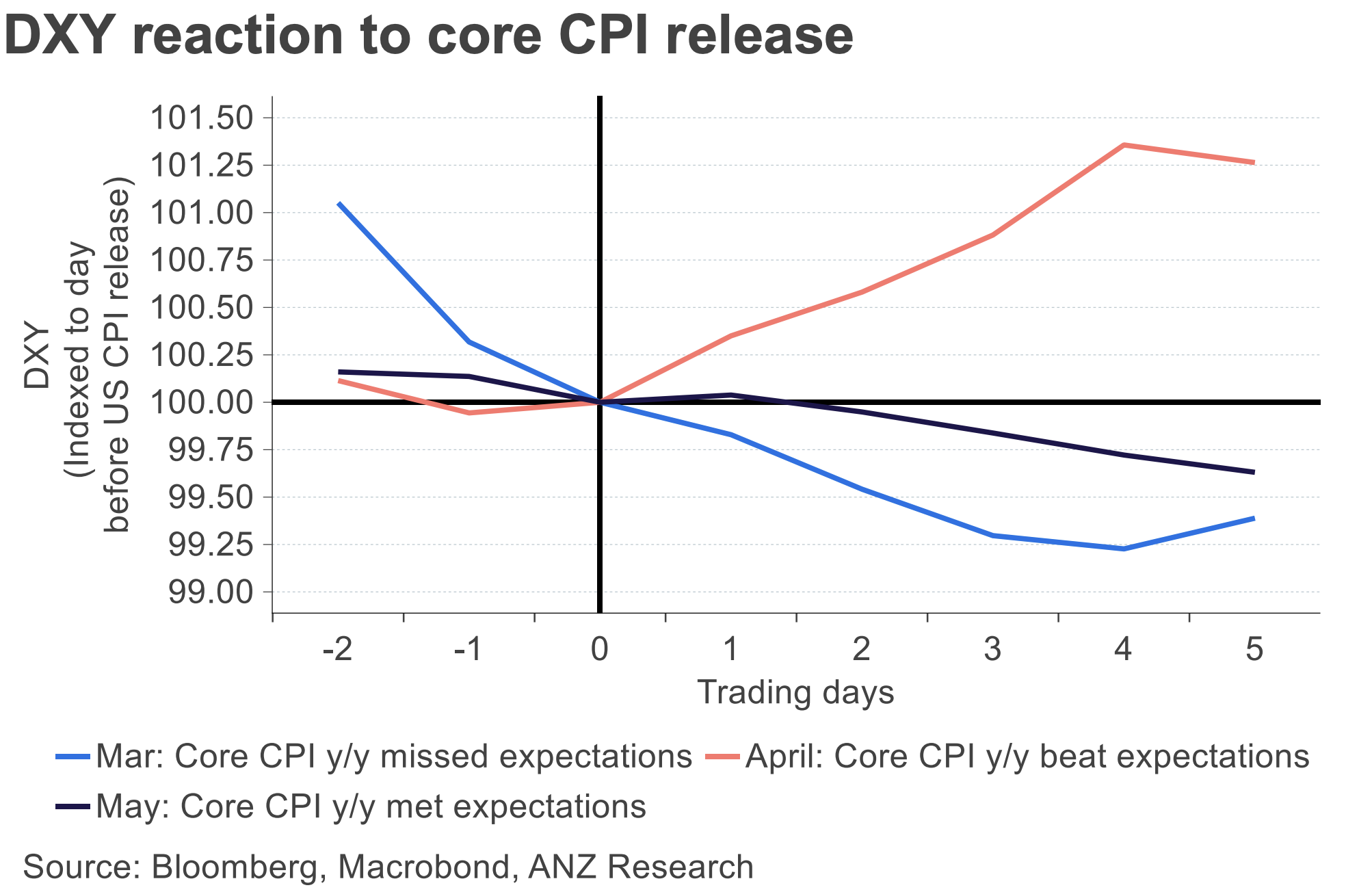

ANZ Research previews next week's US June CPI report and the USD outlook around the release.

"Next week’s June CPI release is the key data point ahead of the July FOMC meeting and will determine whether markets build additional Fed tightening expectations or extend the recent consolidation. Markets are likely to look through any energy-driven boost to headline inflation if underlying price pressures remain contained," ANZ notes.

"Scenario 1: CPI in line with or below expectations (base case) Lower energy prices and easing geopolitical risks have reduced near-term inflation pressures. As such, a CPI print in line with or below expectations is unlikely to meaningfully shift Fed pricing. Also, we expect June’s core CPI to have risen by 0.2% m/m, leaving annual core inflation at 2.8% y/y. While inflation data may remain volatile in coming months, an in-line June outcome should be largely a non-event for the USD and keep the DXY broadly confined to its recent 100.5–101.5 range.

Scenario 2: CPI above expectations A stronger-than-expected core CPI print would reinforce concerns that inflation remains sticky and prompt markets to bring forward or increase Fed tightening expectations. This would support the USD. This can take the DXY towards touching 102, particularly if followed by a firm PPI print, increasing confidence in a more hawkish Fed path. CFTC non-commercial positioning show that net longs have increased. EUR longs continue to decline, while most other G10 currencies remain net short, underscoring the market's preference for the USD," ANZ adds.