eFX Apex

The Institutional-Grade Data Hub

- Plus: Discretionary Trades

- Edge: Sentiment Trades

- Alpha: Systematic Trades

- Apex: Full Big Data Stream

• NZD/USD up 0.3% on higher-than-expected New Zealand inflation

• Q2 inflation at 4.1% y/y, above analysts' forecasts of 4.0%

• Data reinforces expectations of further RBNZ rate hike

• Westpac expects further rate hikes at the Sept, December rate meetings

• NZD set for a retest of 0.5863, a one-month high; break opens 0.5900-10

• Support 0.5825-30, 0.5800-05; Asia range 0.5853-0.5859

NZD:

(Krishna Kumar is a Reuters market analyst. The views expressed are his own.)

• Seems little in way of movement in USD/JPY during Tokyo's long weekend

• USD/JPY remains relatively weak, still in stasis on 162, 162.49-50 EBS today

• Essentially sideways since July 6, between 161.28 July 10, 162.71 July 8

• Wider 160.49 low July 3, 162.84 high July 1 parameters into the fall?

• Threat of Japan FX intervention still on tries higher

• Hawkish Fed expectations, Middle East war, good Tokyo FX demand supportive

• JGB-US Treasury rate differentials narrower, in 2s @269, 10s @183 bps

• Technically, USD/JPY holding above its 162.26-37 ascending hourly Ichi cloud

• Flat hourly kijun ahead of cloud at 162.41, 100/200-HMAs 162.31/23 in/below

• Nearby option expiries today 162.00-30 $1.4 bln, 162.50-75 $504 mln

• Massive $5.9 bln above between 163.00-50, below $1.4 bln between 161.25-75

• Related comments , , ,

• And , also , on US-Iran ,

• US markets , , ,

USD/JPY daily:

USD/JPY hourly:

NYMEX WTI crude oil futures:

(Haruya Ida is a Reuters market analyst. The views expressed are his own)

• AUD/USD opens 0.25% higher despite broadly stronger U.S. dollar

• Risk aversion, higher oil prices, U.S-Iran escalation taken in stride

• Rally despite higher Treasury yields impressive; U.S. 10-year yield up 5bps

• 38.2% Fibo of May-June drop at 0.7023 continues to cap AUD rise

• AUD/NZD recovers from a near 4-month low hit Mon; Tue NZ Q2 CPI key

• AUD rally continues to be capped by 38.2% Fibo of May-June drop at 0.7023

• Strong support at 0.6960-65; Monday range 0.6960-0.7014

AUD:

(Krishna Kumar is a Reuters market analyst. The views expressed are his own.)

Danske Research maintains a bullish forecasts profile for USD/CAD targeting the pair at 1.43 in 6-months, and 1.46 in 12-months.

"The Bank of Canada (BoC) held its policy rate at 2.25% in July, judging the current stance appropriate amid two-sided risks. We expect the BoC to stay on hold through 2026 while the Fed hikes in December, leaving front-end rate differentials in favour of the USD. Markets price close to one BoC hike by YE.," Danske notes.

"We keep an upward-sloping USD/CAD profile, supported by still-wide rate differentials and our structurally constructive USD view. Near-term CAD support from higher energy prices and stretched long-USD positioning is possible but should fade as energy markets stabilise," Danske adds.

(Updates to afternoon trading)

• Dollar largely steady as Iran war keeps markets cautious

• Brent crude futures pare earlier gains

• Burnham names Healey as finance minister

By Chuck Mikolajczak

NEW YORK, July 20 (Reuters) - The dollar rose on Monday as investors weighed contradictory developments in the Iran war, while the pound fell from earlier levels as markets prepared for new British Prime Minister Andy Burnham.

Yemen's Iran-aligned Houthis said they were imposing a naval blockade on Saudi Arabia, a move that opens a new front against the United States in its war on Iran and widens the threat to global energy supplies and trade beyond the Gulf.

But crude prices came off their initial move higher as Iran and the United States signaled they wanted to resume diplomacy.

U.S. crude advanced 0.22% to $82.67 a barrel and Brent rose to $88.78 per barrel, up 0.77% on the day, after earlier hitting their highest levels in more than a month.

The dollar index , which measures the greenback against a basket of currencies, climbed 0.18% to 100.92, with the euro down 0.19% at $1.1417.

"There's a lot of conflicting news coming from the Middle East — on one hand, it looks like it could be escalating, on the other hand, it looks like there's another ... last-ditch effort to try to like get a new ceasefire and that's why oil came off," said Marc Chandler, chief market strategist at Bannockburn Capital Markets in New York.

The economic calendar for the week is light, and Federal Reserve officials are in a "blackout period" of public comments ahead of the central bank's meeting next week. Recent reports on U.S. inflation and the labor market have caused markets to sharply curb expectations for a rate hike from the Fed next week, pricing in only a 16.6% chance for an increase, according to CME FedWatch, down from more than 40% a week ago. Expectations for a hike at the September meeting are at 62.8%, however.

A bevy of Fed officials, including Chairman Kevin Warsh, have flagged concerns about inflation pressures in recent weeks while noting the labor market remains stable.

The European Central Bank (ECB) will hold a policy meeting later this week, with markets pricing in only a 13.1% chance of a hike, according to LSEG data, with a 78% chance for an increase at its September meeting.

The ECB is seen as being more likely to be aggressive in raising rates than the Fed due to the sensitivity to energy prices in the region and its single mandate of price stability.

UK CHANCELLOR CHOICE IN FOCUS

Sterling weakened 0.12% to $1.3437 after climbing to $1.3481 as Burnham took over from Keir Starmer, becoming Britain's seventh Prime Minister in a decade as he pledged to reshape the country's politics and deliver a new economic model.

The pound pared declines after Burnham named John Healey as finance minister from a session low of $1.341.

UK assets last week were supported by reports that the job would likely go to Shabana Mahmood, widely regarded as a centrist, rather than a more left-leaning candidate.

"Markets have delivered their first verdict on Andy Burnham, which is cautious optimism. Investors appear comfortable with the idea of a more active government, but only if it can deliver faster economic growth without stretching the public finances," said Lale Akoner, global market strategist at eToro. Elsewhere, the U.S. dollar was down 0.14% at 6.769 against the Chinese yuan in offshore trade after China kept its benchmark lending rates unchanged for a 14th consecutive month on Monday, in line with market expectations.

Against the yen , the dollar edged up 0.03% to 162.46

in thin liquidity as Japan observed the Marine Day holiday.

<^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^> (Reporting by Chuck Mikolajczak, additional reporting by Sophie Kiderlin in London and Gregor Stuart Hunter in Singapore; Editing by Jamie Freed, Andrei Khalip, Andrew Heavens, Will Dunham and Susan Fenton) ((; @chuckmik.bsky.social))

• NY opened near 0.7005 after 0.6960 traded overnight, the rally extended

• Rallies in silver, copper, equities & gold's upward mover helped lift AUD/USD

• The pair hit 0.7015 but bulls could not maintain upward momentum

• USD buying & firmer yields weighed on the pair

• 0.6995 neared before the pair settled near 0.7005 late, it was up +0.32% late

• AUD/JPY's rally helped to keep AUD/USD higher on the session

• Techs lean bullish; RSIs rising, 10-DMA supports, pair

above t-l off May 13 high

audusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

Goldman Sachs sees good value in CHF funding on a three-month basis

"USD/CHF offers exceptional levels of carry for a pair that has acted as a clear risk-hedge in this environment, which we think places it as an attractive portfolio hedge in an environment where energy shock risks are still simmering. At the same time, CHF's gold connection is also the clearest risk to the case for funding in our view," GS notesa.

"We continue to see a pivot back to a neutral CHF intervention bias by the SNB as another potential route to Franc outperformance, though after the SNB's weak tweak in June, this process appears to us to be a more gradual one. We see good value in CHF funding on a three-month basis where these key risks appear more remote, offering greater carry in G10 crosses than the more typical choice of the Yen," GS adds.

Sterling's near-term prospects look relatively upbeat as the pound consolidates recent gains, near 1.3450, as Andy Burnham became Britain's seventh prime minister in a decade with a pledge to change politics.

The currency was trading just below mid-July highs at 1.3556 and well above late-June lows in the mid-1.31s, suggesting stability near trend highs. With summer liquidity issues prevailing, sterling is likely to hover around its flattening daily cloud near 1.3420.

As the market assesses Burnham's initial moves as head of government, GBP traders and the broader FX market will stay focused on the fluid Middle East situation and its effects on oil, macro themes, and downstream UK inflation, growth and fiscal dynamics.

Fiscal concerns will also remain a focal point. While Burnham has said he will honor fiscal rules, he has set ambitious goals to tackle homelessness, while also building more public housing to help bring down welfare spending, which would help fund higher defense investment. For now, UK macro traders appear willing to give Burnham a chance. But if geopolitical ructions lift oil toward late-March highs above $100/bbl, the new prime minister may face difficult spending decisions, which will spotlight gilt yields as a fiscal sustainability barometer.

Technically, a dip below the flat 200-DMA at 1.34 would put

the July 8 low at 1.3323 in sharper focus; a rise in UK 10-yr

gilts above 5.2% could lead bears to target the mid-1.31s.

Sterling Chart:

(Paul Spirgel is a Reuters market analyst. The views expressed

are his own)

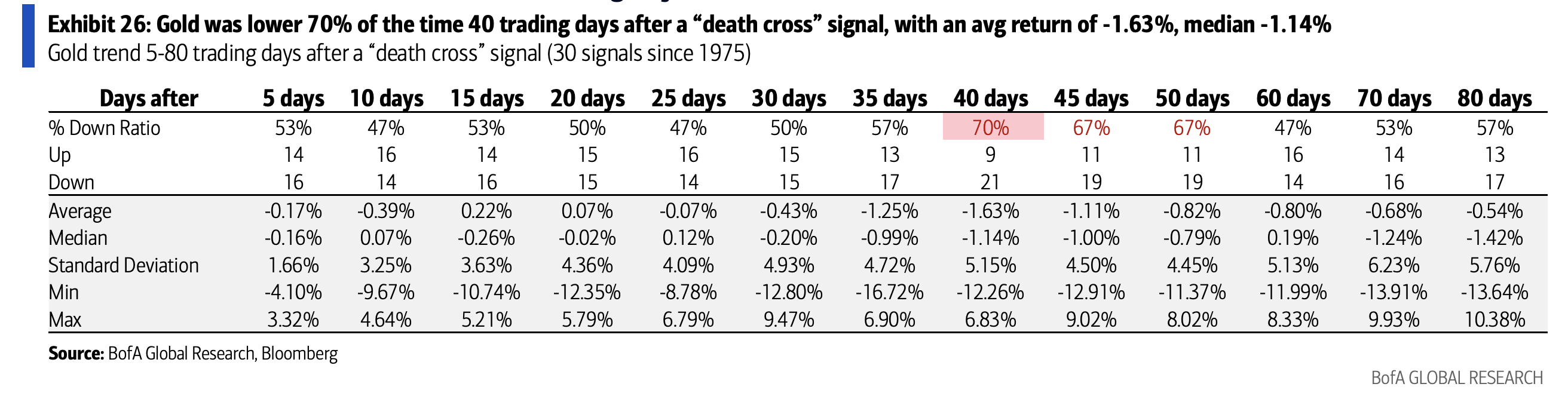

Bank of America Global Research discusses Gold and DXY technical and seasonality outlook and flags a scope further USD gains supported by Gold's death cross signal.

"On June 26, 2026, at $4,088.74, gold triggered a “death cross” signal. This is when the 50d SMA crosses below the 200d SMA to imply a downtrend is underway. • After 30 signals since 1975, gold was lower 67-70% of the time 40-50 trading days later with negative average and median returns. This suggests gold may be lower than $4,088.74 around August 24-September 8," BofA notes.

"Gold’s death cross signal implies support and strength for the DXY in the Aug 3-Oct 21 period, with a little more emphasis on late August through September," BofA adds.

• EUR/GBP anchored below 0.8500 as rebound attempts continue to fade on approach to topside resistance

• Recent GBP outperformance leaves scope for upside extension more constrained in the near term

• Positive UK narrative largely in the price - incremental political impulse now diminishing

• Rates market remains skewed hawkish BoE with ~40bps priced by year-end

• Raises the bar for incoming data to validate further GBP strength (labour market, CPI due Tue/Wed)

• Initial resistance: 0.8520–22 (200H MAs), break would likely encourage dip buyers

• Support: 0.8455 (15 Jul low), then 0.8400

EURGBP hourly chart

Justin McQueen is a Reuters market analyst. (The views expressed

are his own).

((Email: ))

Morgan Stanley Research adopts a neutral to slightly bullish bias on EUR in the near-term.

"We see modest near-term idiosyncratic upside risks to the EUR, as our economists see the ECB tone as likely to keep a September hike on the table. They note risks that core inflation moves up in 3Q26, as the ECB expects. A relatively hawkish tone from President Lagarde this week would likely solidify hiking expectations, potentially leading investors to seek alternative funders for long EM carry trades," MS notes.

"One potential near-term catalyst is the July 24th expiry of across the-board US tariffs. The absence of any announcement of 232 or 301 replacements (as expected) may boost EUR, as data from Yale Budget Lab suggest that the effective tariff rate on Germany may fall over 3 percentage points in the absence of the section 122 surcharge, more than a number of other developed economies," MS adds.

• AUD/USD fell below the 10-DMA, hit a 4-session low of 0.6960

• Buyers then emerged, the pair rallied above the 10-DMA, turned positive

• Rallies in gold, silver, copper & equities helped the pair make gains

• Pair got an added boost as USD, USD/CNH, oil fell on possible US-Iran negotiation

• Friday's high broke, Thursday's high was neared, 0.7008 traded into NY's open

• AUD/USD traded up +0.37% in early action which helped techs lean bullish

• RSIs are rising & AUD/USD moved back above the trend line off the May 13 high

• The 0.7020/25 area is key short-term resistance bulls need

to overcome

audusd

(Christopher Romano is a Reuters market analyst. The views

expressed are his own)

• EUR/USD-0.05%, USD/JPY 0.04%, GBP/USD 0.06%, AUD/USD 0.24%

• S&P E-minis 0.26% , DAX 0.29% , Nikkei -4.3% , FTSE-100 -0.4%

• GBP/USD range bound below 1.35 with event risk in focus

• A bullish AUD/USD skew hinges on a key Fibo breakout

• EUR/USD traders unconvinced by the bounce

• USD/JPY-Tight ranges persist as grind higher stalls ahead of cycle high

• FX option expiries U.S. Open (Peter Stoneham is a Reuters market analyst. The views expressed are his own) ))

• USD/JPY muted, holding within a tight 162.31-162.60 band

• Spot easing off intraday highs alongside softer oil in London trade

• Iran signals potential willingness to pursue negotiations with the U.S.

• Macro backdrop still USD/JPY supportive - subdued FX vol underpinning carry demand

• But upside still constrained by persistent intervention risk, particularly ahead of 162.84

• Resistance: 162.84 through to 163, support at 162.00-05

(21-day MA), 160.70

USDJPY daily chart

Justin McQueen is a Reuters market analyst. (The views expressed

are his own).

((Email: ))

(Repeat changes tense for the week ahead ) Billions of euros in FX option strikes around the low 1.14s have helped cap and underpin EUR/USD in recent weeks — a reminder that, while not an exact science, large impending option expiries can influence the spot market as they approach. EUR/USD has edged up a touch since Tuesday's softer-than-expected U.S. CPI data, but it remains well entrenched within a long-standing 1.1400-1.1500 range, with plenty more option strike expiries within those parameters likely to keep shaping price action this week.

Traders using FX options to trade volatility are also heavily involved in the cash market, and as an option expiry approaches — 10 a.m. New York (1400 GMT) for G10 currency pairs — hedging flows will typically increase as the cash-versus-option relationship becomes more crucial to profit and loss. If an option is likely to be exercised, the opposing party may need to buy or sell more of the underlying currency to meet their obligation. These flows can often drive spot towards the nearest and largest strikes, adding to any nearby support or resistance and helping to contain price action until those strikes expire.

Monday, July 20, sees the largest strike expiries with almost 10 billion euros in a 1.1385-1.1510 range

Tuesday, July 21 brings 1.1400 expiries worth 2.3 billion euros, alongside 1.1445-50 (1.6 billion), 1.1470-85 (4.3 billion) and 1.1500 (2 billion). Wednesday, July 22 has 1.1400 expiries on 3.3 billion euros and 1.1490-1.1500 on 1.2 billion, while Thursday, July 23 sees 1.1400-10 (1.1 billion), 1.1450-65 (3.2 billion) and 1.1500-10 (2 billion). The lack of spot volatility within a familiar range is also weighing on FX option premiums - with EUR/USD implied volatility languishing close to multi-year lows.

Related comment - FX clues from the options market

EUR/USD OTC FX option strikes expiring July 17-2

(Richard Pace is a Reuters market analyst. The views expressed

are his own)

• EUR/USD reached 2026 low at 1.1325 in June

• Pair then bounced to reach 1.1472 on July 2

• Traders continued to pare longs

• Net short ($2.3 billion) emerged on July 7

• Net short was trimmed to $1.8bln week Jul-7-14

• EUR/USD 1.1482 Jul 15, dropped to trade 1.1424-45 Jul 20

•

EURUSD

(Jeremy Boulton is a Reuters market analyst. The views expressed

are his own)

• Shares of Australia's Aurelia Metals up 5.7% at A$0.285, on track for their strongest session since June 15, if trend holds

• Mining and exploration co posts FY26 gold production of 50.4 koz, above top end of forecast range of 45-50 koz

• About 6.5 million shares trade hands, 1.8x 30-day average

• YTD, stock up 13%, including session's moves

(Reporting by Subhalakshmi Dey in Bengaluru)

• Shares of Australia's Rumble Resources rise as much as 4.4% to A$0.047, its highest level since July 7

• Precious metals explorer says drilling at its Munarra Gully project in Western Australia (WA) intercepted high-grade gold and copper

• Co adds, planning underway for a targeted drilling campaign

• Stock down 12% YTD, including session moves

(Reporting by Shravya Marakini in Bengaluru)

• AUD/USD up 0.15% in Asia after trading in a 0.6960-0.6995 range

• Opened 0.6976 from Fri 0.6981 close, dipped to day low on Iran escalation

• U.S. strikes Iran for 9th day; allies in region report fresh attacks

• Dip-buyers emerge as 0.6960-65 support holds, rally back to day high ensues

• Failure at 38.2% Fibo of May-June drop at 0.7023 last Wed continues to weigh

• AUD/NZD risks further drop as key data loom; NZ Q2 CPI Tue, AU June jobs Thu

• Support 0.6960-65, 0.6935-40, resistance 0.6995-0.7000, 0.7020-25

AUD:

AUDNZD:

(Krishna Kumar is a Reuters market analyst. The views expressed are his own.)

• GBP/USD cautiously higher, last 1.3451, as USD abates broadly

• Tentatively finds a bottom around 1.3445, a key technical floor

• Bollinger uptrend channel base and Ichimoku cloud merge to support

• If they crack, next ledge at 100 and 200 DMA near 1.3400 to be tested

• Burnham set to take over as PM; finance minister eyed

• Choice for crucial role may dictate steling's next big

move

GBP

(Ewen Chew is a Reuters market analyst. The views expressed are

his own.)

• Australian gold stocks fall as much as 1.4% to hit their lowest since June 11

• Sub-index on track for a fourth straight session of losses

• Bullion prices posted their biggest weekly loss in six on Friday as escalating U.S.-Iran tensions fuelled inflation fears and reinforced expectation for U.S. interest rate hikes [GOL/]

• Evolution Mining and Northern Star Resources

drop 2.3% and 0.9%, respectively

• Sub-index down 24.1% YTD

(Reporting by Keshav Singh Chundawat in Bengaluru)

• EUR/USD glides lower to 1.1425 from 1.1433, nearing chart pivot

• 21 DMA at 1.1414 about to be tested, as UST yields set to rise

• Could break lower and into Bollinger downtrend channel 1.1385

• Mon close below that will engage bearish technical momentum

• Oil prices spiking again as US-Iran conflict escalates

• US launches ninth consecutive night of attacks on Iran

EUR

(Ewen Chew is a Reuters market analyst. The views expressed are

his own.)

• USD/JPY up 0.1% in Asia as U.S.-Iran conflict escalates

• U.S. renews Iran strikes; allies in the region report more Iranian attacks

• U.S. crude futures up 3% to a more-than-one month high, undermine JPY

• Traders remain on intervention alert with Japanese markets closed Monday

• Tokyo may exploit thinner liquidity to bolster the yen

• Japan to leave monetary policy tools to BOJ in economic blueprint-document

• Resistance 162.75-85, 163.00, support 162.00-10, 161.50-60

• Friday range 162.13-162.52, Asia 162.41-162.59

JPY:

(Krishna Kumar is a Reuters market analyst. The views expressed are his own.)

• AUD/USD -0.2% in early Asia as US renews strikes on Iran

• U.S. allies in the region report more Iranian attacks on Sunday

• Risk aversion undermines AUD; Wall Street declines Fri as chips sell off

• U.S. crude futures rally to a more-than-one month high, sap risk appetite

• Failure at 38.2% Fibo of May-June drop at 0.7023 last Wed continues to weigh

• Support 0.6960-65, 0.6935-40, resistance 0.6990-0.7000, 0.7020-25

• Friday range 0.6966-0.7000, 0.6965-0.69765

AUD:

(Krishna Kumar is a Reuters market analyst. The views expressed are his own.)